Balanced scorecard (BSC) is a methodology for measuring the performance and efficiency of an organization by tracking a balanced set of indicators: financial and non-financial. The distinctive features of this system are:

- focus on the implementation of the company’s strategy, while helping to manage operational activities

- definition of a set of measurements in accordance with the set goals to track the result

- combination of financial and non-financial measures

- introduction of corrective actions in case of deviation from the intended goals

Balance

The main meaning is contained in the word balance. Previously, business owners evaluated the state of their firm only from a financial point of view, but with the change in time and approaches to business, it became clear that this data is not enough, so there was a need to track non-financial side.

Financial indicators often have monetary values as a unit of measurement. Traditionally, financial measures include revenue, margin income, profit, debt, etc., usually, all these figures are included in the financial report. Everything that is not included in this report relates to non-financial indicators, such as production time, product quality, product delivery, customer satisfaction, customer service, etc. For an objective assessment of the state of affairs in the organization, it is necessary to combine financial and non-financial indicators, as well as to mix them correctly.

The first attempt to combine financial and non-financial indicators to track the company’s progress was made by Art Schneiderman in 1987. Based on the work of Art Schneiderman, David Norton and Robert Kaplan developed this topic and wrote an article that was published by the Harvard Business Review in 1992. Then David Norton and Robert Kaplan wrote the book “The Balanced Scorecard”. The authors used articles and books to widely spread the concept of a balanced scorecard, so later they were considered as the creators of this approach.

At the moment, there are different approaches to the development of BSC, they can be conditionally united into several groups, which are usually called generations since the division is based on the years of their appearance.

First Generation

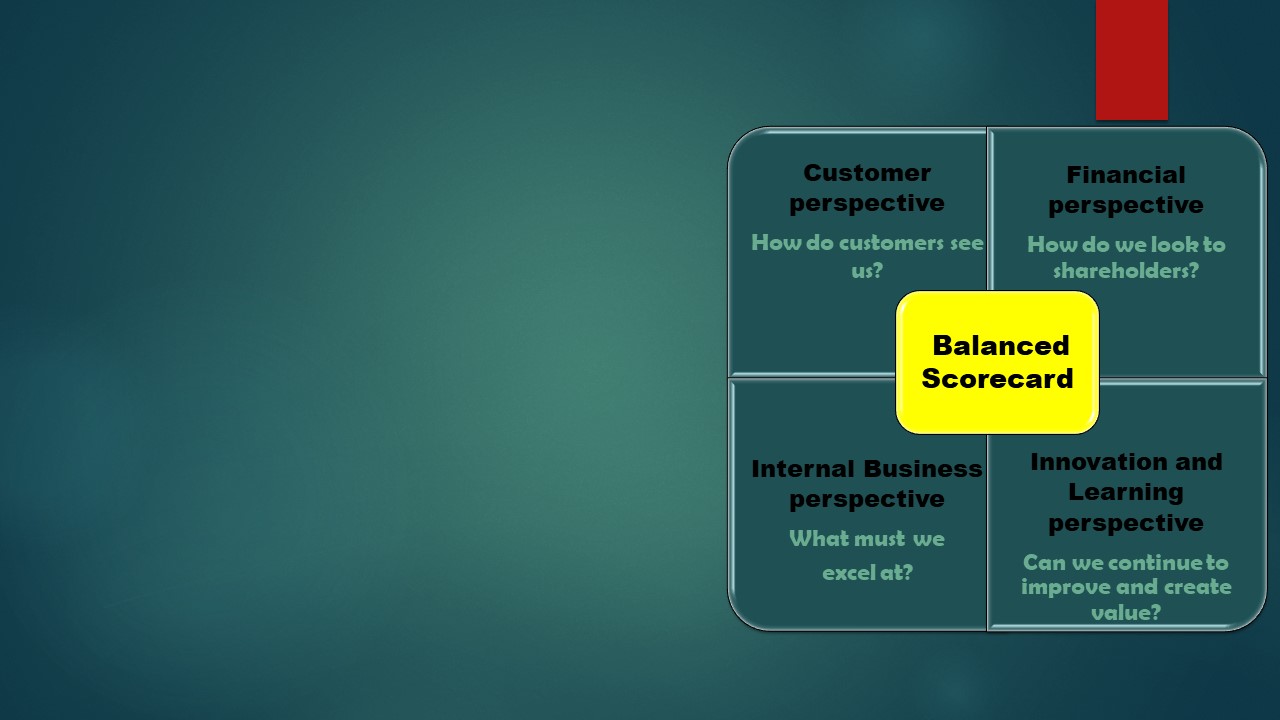

Initially, Robert Kaplan and David Norton proposed a balanced scorecard approach based on measuring the four main areas of a business, commonly referred to as perspectives. These are financial, customer, internal business processes, and innovation and learning.

Financial Perspective

This category answers the question “How do we look to shareholders?” and it is characterized by the analysis of the financial measures of the organization: revenue, profitability, cash flow, sales growth, operating income, as well as the use of financial resources. We have already mentioned that previously financial indicators were the main starting point for evaluating companies, then some critics said that finance should be put on the back burner, so if non-financial indicators are improved, then, accordingly, income will grow. But in real life, this point of view turned out to be unviable. A well-designed financial control system will help to improve, rather than hinder, the development of the organization. Do not exclude this indicator, it is necessary to combine it correctly with other indicators.

Customer Perspective

This category answers the question “How do customers see us?” and is based on the needs and interests of the client. An important indicator is customer satisfaction. There are four areas that are most important to the consumer and that need to be constantly improved. These are time, quality, performance and service, and cost. For the BSC to produce results, it is necessary to formulate specific goals that relate to these areas, and then translate these goals into measures to implement them.

Internal Business Perspective

This category answers the question “What must we excel at?” and it is focused on improving the internal business processes of the organization, as they can help in customer satisfaction. Therefore, it is worth paying the most attention to those business processes that are directly related to customer satisfaction, such as production time, delivery time, product quality improvement, employee skills, pricing policy, etc. The company should determine which processes and competencies they should identify and specify the dimensions for them.

Innovation and Learning Perspective

This category answers the question “Can we continue to improve and create value?” and refers to the improvement of existing products, the development of new products, the company’s ability to innovate, the improvement of staff skills, etc.

First-generation BSCs are more suitable for small and medium-sized companies and are not quite applicable for large companies or the public sector, as well as for non-profit organizations. Therefore, there was a need to modify this version.

Second Generation

The second generation of BSC is characterized by the creation of strategic maps with strategic objectives. The idea of making strategic maps was also suggested by Robert Kaplan and David Norton in their later works. But in their work, they also started from four business perspectives, within which they set strategic objectives (each goal is displayed as text written in a graphic figure), and then determined the cause-effect chain between these objectives (usually displayed with arrows). It turns out a strategic linkage model. With the help of the strategic map, it became easier to visualize strategic objectives, as well as to track the results of activities. To do this, at least one Key Performance Indicator (KPI) must be defined for each goal. KPIs monitor the implementation and effectiveness of the organization’s strategies, as well as indicate the difference between actual and target indicators.

Since a limited number of perspectives were not suitable for all organizations, versions of strategic maps began to appear, with a different number and set of perspectives that best suited the needs of organizations. But despite these changes, the standard set of perspectives remains the most common option for making strategic maps.

Third Generation

The reason for the appearance of the third generation of the balanced scorecard was the difficulty of creating the cause-effect chain between a large number of strategic objectives. This approach is characterized by the introduction of the concept of Destination Statement, which describes the final result of the company’s strategy if this strategy is successfully implemented, that is, the result that the company strives for. The process is as follows: first, you create a Destination Statement, then, based on this document, you define the strategic activities and the strategic objectives for its implementation. Once strategic objectives are set, they are assigned a master who determines specific measures to achieve them, as well as indicators to track these goals.

Balanced scorecard design methods continue to evolve and adapt to the needs of different companies, as well as to improve usability. At the moment, software for working with BSC has been developed, they include various functions, such as strategic mapping, reporting, tracking KPIs, communication tools, etc.

Find more analytical and strategic marketing information to improve your business performance in the corresponding sections of the website.